The 50/30/20 budget rule is one of the most practical ways to bring order to your money without turning your life into a spreadsheet. It gives you a simple, flexible framework: half of your take-home income for true essentials, roughly a third for lifestyle choices, and the rest for building your future. Because the 50/30/20 budget rule focuses on big buckets rather than every tiny purchase, it’s easier to start, easier to stick with, and far less stressful than hyper-detailed budgets.

Most people don’t fail at money because they can’t do math—they struggle because the plan they’re trying to follow is too rigid. You can white-knuckle a no-fun budget for a few weeks, but eventually real life wins. The 50/30/20 budget rule works precisely because it makes room for the human part: you still get to enjoy wants, you still cover needs, and you still make steady progress toward savings and debt goals.

Contents

- 1 What Is the 50/30/20 Budget Rule?

- 2 Why This Rule Works

- 3 How to Apply the Rule Step by Step

- 4 The 50%: Needs (How to Keep Them in Check)

- 5 The 30%: Wants (Enjoy—With Guardrails)

- 6 The 20%: Savings and Debt (Where Progress Happens)

- 7 Real-Life Examples (Seven Scenarios)

- 8 Adapting the Rule Without Breaking It

- 9 Advanced Tactics That Pair Well With 50/30/20

- 10 Common Mistakes (and Fixes)

- 11 How to Calculate Your Numbers Fast

- 12 Frequently Asked Questions

- 13 30-Day Implementation Plan

What Is the 50/30/20 Budget Rule?

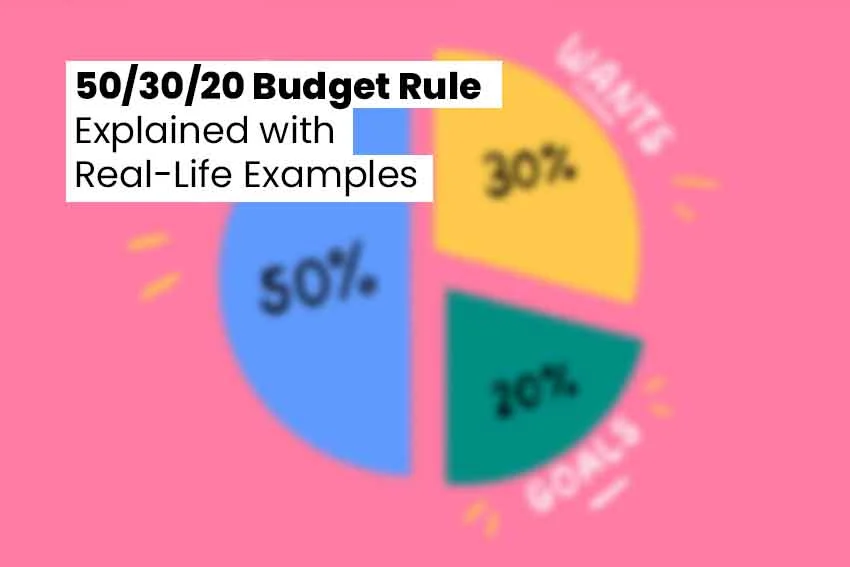

At its core, the 50/30/20 budget rule divides after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings or debt repayment. Under the 50/30/20 budget rule, “needs” are non-negotiables—housing, utilities, groceries, basic transportation, insurance, and minimum debt payments. “Wants” are quality-of-life upgrades such as dining out, travel, streaming, hobbies, and nicer (not necessary) upgrades. “Savings and debt” covers your emergency fund, retirement contributions, investments, and extra payments on loans.

Why This Rule Works

The 50/30/20 budget rule reduces decision fatigue. Instead of asking “Can I afford this?” every day, you set guardrails once a month and live inside them. It’s also highly adaptable: if your income rises, the same percentages scale; if your costs spike, you adjust the mix without throwing out the plan. Finally, it encourages balance: you enjoy the present without sacrificing the future.

How to Apply the Rule Step by Step

1) Determine Your After-Tax Income

Use your net pay—the money that actually hits your account. For freelancers or commission earners, average the last 6–12 months and use the lower end to be safe. A steady base makes the 50/30/20 budget rule feel predictable instead of brittle.

2) Map Your Current Spending Into the Three Buckets

Pull the last 60–90 days of bank and card statements. Highlight essentials (needs), lifestyle (wants), and future-focused items (savings/debt). Many people are surprised by how much “leaks” into wants—subscriptions, takeout, convenience purchases. That’s good news: leaks are easier to fix than rent.

3) Do the Math Once, Then Automate

If you bring home $4,000, the 50/30/20 budget rule suggests $2,000 for needs, $1,200 for wants, and $800 for savings/debt. Set up automatic transfers on payday: bills to a “needs” account, fun money to a “wants” account, and the rest to savings/investments. Automation is the cheat code.

4) Recheck Monthly, Fine-Tune Quarterly

Budgets are living documents. Review category totals monthly; every quarter, decide if housing, insurance, or subscriptions need renegotiating.

The 50%: Needs (How to Keep Them in Check)

Needs include rent or mortgage, utilities, groceries, transportation, insurance, childcare, and minimum loan payments. If your needs exceed 50%, you’re not failing the 50/30/20 budget rule—you’re seeing reality clearly. Use that clarity to:

- Tackle the big rocks: housing and transportation. Could you downsize, refinance, get a roommate, switch to a cheaper car or public transit a few days a week?

- Shop your bills annually. Internet, phone, and insurance can often drop 10–20% with a single call or a switch.

- Keep groceries simple. Plan meals, buy generics, batch-cook, and use up what you have before shopping again.

- Build sinking funds for inevitable costs (car maintenance, annual premiums) so they don’t blow up a month.

The 30%: Wants (Enjoy—With Guardrails)

Wants keep motivation high. The trick is prioritizing what you truly enjoy and trimming the rest. Try a 48-hour delay on nonessential purchases. Rotate streaming services instead of paying for all at once. Bundle experiences with friends (host game nights, hike, free events). If the wants bucket is tight, use a swap rule: add one new luxury only if you remove another.

The 20%: Savings and Debt (Where Progress Happens)

This is the engine of your financial future. Start with a mini emergency fund (one month of expenses), then target 3–6 months. Contribute to retirement (especially if you get an employer match), and prioritize high-interest debt. The 50/30/20 budget rule makes this simple: the 20% is non-negotiable. Automate transfers on payday so saving happens before spending.

Real-Life Examples (Seven Scenarios)

Sarah, 26 — First Apartment

Take-home: $3,200. Using the 50/30/20 budget rule, she sets $1,600 for needs (rent, metro pass, groceries, phone), $960 for wants (restaurants, yoga, streaming), and $640 for savings/debt (emergency fund + extra student loan payments). After three months, she sees groceries creeping up; she switches to meal planning and brings wants back in line without feeling deprived.

Average net: $3,800 (variable). He runs the 50/30/20 budget rule on his lowest three-month average to stay conservative: $1,900 needs, $1,140 wants, $760 savings/debt. In peak months, any surplus above those caps goes straight to a “slow months” buffer, so volatility stops wrecking his budget.

Priya & Luis, 31 and 33 — New Homeowners

Net: $6,500 combined. Mortgage and daycare stretch needs to 55%. They adapt the 50/30/20 budget rule to 55/20/25 for a year: trim wants to $1,300, push savings/debt to $1,625. When daycare drops next year, they’ll slide back toward 50/30/20 and boost retirement contributions.

Maya, 29 — High-Cost City Renter

Net: $4,400; rent is $2,000. She adopts a temporary 60/20/20 version of the 50/30/20 budget rule while she hunts for a roommate and negotiates internet/insurance. Within six months, needs fall to 52%—close enough that the next raise will restore balance.

Owen, 41 — Debt Snowball Sprint

Net: $4,700. He keeps needs at 50% and limits wants to 25% for a year, pushing 25% to savings/debt under a slightly modified 50/30/20 budget rule. The extra 5% crushes his last credit card in nine months, freeing up cash flow permanently.

Aisha, 38 — Single Parent

Net: $3,900. Childcare makes needs 58%. She leans on community resources (library, free events) to keep wants modest, and uses the 50/30/20 budget rule framework to direct tax refunds into her emergency fund, reaching 3 months of expenses in a year.

Diego, 52 — Late Starter on Retirement

Net: $5,600. He keeps needs to 48%, wants to 22%, and pushes 30% to savings/debt for two years—a purposeful twist on the 50/30/20 budget rule. Catch-up IRA contributions plus extra mortgage payments move the needle fast.

Adapting the Rule Without Breaking It

High-cost areas, heavy debt loads, or unpredictable income don’t disqualify you. They just mean you’ll bend the 50/30/20 budget rule (temporarily) while you work a longer plan. If needs sit at 60%, aim to reduce them by one or two percentage points each quarter. If income swings, base your plan on a conservative average and shovel all surplus into savings at month end. The 50/30/20 budget rule is a compass, not handcuffs.

Advanced Tactics That Pair Well With 50/30/20

- Three-account system: open separate checking accounts for needs and wants, plus a savings account. Route paycheck splits automatically so you don’t “accidentally” spend savings.

- Pay-yourself-first stacking: on payday, fund savings/investments first, then bills, then wants. The 50/30/20 budget rule becomes effortless when the order protects your priorities.

- Sinking funds: set up mini buckets for car repairs, travel, gifts, medical, and annual premiums. Scheduling these prevents budget blowups.

- Seasonal recalibration: do a spring and fall audit—insurance quotes, utility usage, subscription inventory, and grocery patterns.

- Raise rule: when income rises, dedicate at least half of the increase to the 20% bucket for six months before upgrading lifestyle.

Common Mistakes (and Fixes)

1) Calling Wants “Needs”

A reliable car is a need; a luxury trim is a want.

Fix: write a one-line definition of each for your situation and keep it on your phone.

2) Ignoring Annual/Irregular Bills

They’re predictable—just not monthly.

Fix: total them and divide by 12; move that amount to a sinking fund monthly.

3) Budgeting to the Penny in Wants

Perfection creates rebellion.

Fix: give yourself a flexible wants cap—once it’s gone, it’s gone.

4) Lifestyle Creep After a Raise

New money disappears fast.

Fix: run the new numbers through the 50/30/20 budget rule and automate the savings increase before you see it.

5) Never Reviewing the Plan

Stale plans drift.

Fix: 20-minute monthly check-ins; 60-minute quarterly tune-ups.

How to Calculate Your Numbers Fast

- Add up last month’s net income.

- Multiply by .50 / .30 / .20 to get targets.

- Categorize last month’s spending into needs/wants/savings.

- Compare actuals to targets; choose one adjustment in each category.

- Automate splits on the next payday so the 50/30/20 budget rule runs in the background.

Frequently Asked Questions

Is the 50/30/20 budget rule realistic on a low income?

Yes, but you may run 60/25/15 or 55/25/20 while you lower housing/transportation or increase income. The key is protecting some savings, even if small.

Where do childcare and health costs go?

They’re needs under the 50/30/20 budget rule. If they push you above 50%, trim other needs or wants and use sinking funds to smooth spikes.

Should I invest if I still have credit card debt?

Prioritize high-interest debt in the 20% bucket, but still capture any employer retirement match—it’s free money. The 50/30/20 budget rule can handle both by sequencing payments.

What about irregular income?

Base the plan on a conservative average. In strong months, keep needs/wants at their caps and push all extra into savings. The 50/30/20 budget rule shines when you automate that overflow.

Absolutely. Pool the net income, agree on needs/wants definitions, and set shared savings goals. Many couples find the 50/30/20 budget rule reduces money fights because expectations are explicit.

How often should I change the percentages?

Infrequently. Small tweaks are fine, but the power of the 50/30/20 budget rule is consistency. Adjust after major life changes (move, new job, baby), not every time a month feels tight.

30-Day Implementation Plan

- Week 1: Gather statements, list bills, and calculate targets with the 50/30/20 budget rule.

- Week 2: Open/label accounts; set up automatic transfers for needs, wants, and savings.

- Week 3: Kill two subscriptions, negotiate one bill, and choose a cheaper default (generic groceries, transit 2×/week).

- Week 4: Build a $500 starter emergency fund, then schedule monthly check-ins for the next quarter.

Money management doesn’t have to be a second job. The 50/30/20 budget rule gives you a blueprint that respects your real life while steadily improving your financial position. You’ll cover the essentials, enjoy intentional treats, and make measurable progress toward an emergency fund, debt freedom, and retirement. If your situation is messy—high rent, variable income, old debts—start where you are. Bend the percentages as needed, keep the spirit of the plan, and let the 50/30/20 budget rule compound small wins into big outcomes. The first month won’t be perfect. That’s normal. What matters is that each month gets a little clearer, a little calmer, and a little more aligned with the life you actually want.

Ready to take the next step? Dive into our Money Management guides for practical budgeting tips, debt payoff strategies, and smarter saving habits — so your money works the way you want:

Explore the Money Management category →